Mortgage Crisis: First-Time Buyers Forced to Take Out 35-Year Mortgages

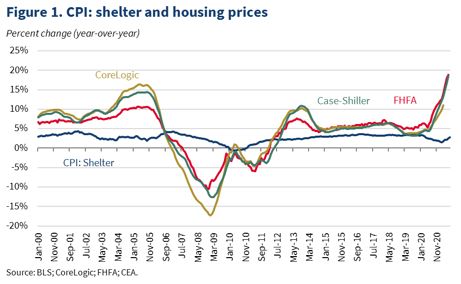

A recent report by UK Finance has revealed that 21% of new first-time buyers are taking out mortgage terms stretching beyond 35 years. This trend is further evidence of the ongoing affordability crunch in the UK housing market, where costs and house prices remain high relative to incomes.

Housing market graph

Housing market graph

According to UK Finance, the proportion of borrowing at up to 40-year terms eased slightly in the first quarter of this year, but remains far higher than in the past. This is particularly significant amongst first-time buyers, who are increasingly needing to take out longer-term mortgages to enter the housing market.

The longer a customer needs to make mortgage payments, the less free income they may have over this period for other important considerations, not least contributions into their pensions. - UK Finance

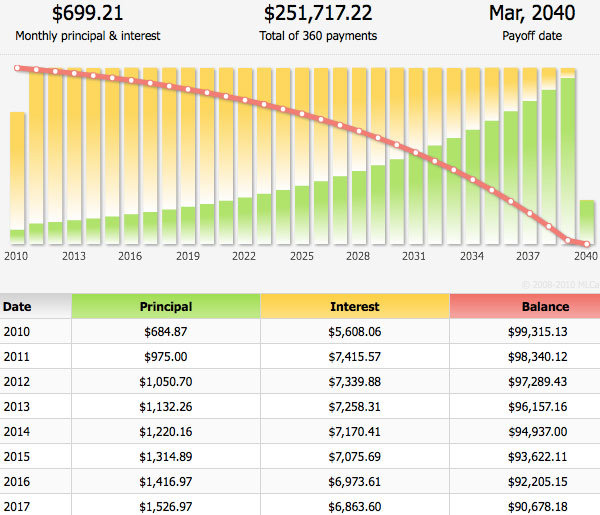

Mortgage payments graph

Mortgage payments graph

Concerns have been raised that some home-buyers could be gambling with their retirement prospects by taking on ultra-long mortgages. Sir Steve Webb, a former pensions minister, obtained freedom of information data from the Bank of England, showing that 42% of new mortgages in the fourth quarter of 2023 had terms going beyond the state pension age.

Retirement graph

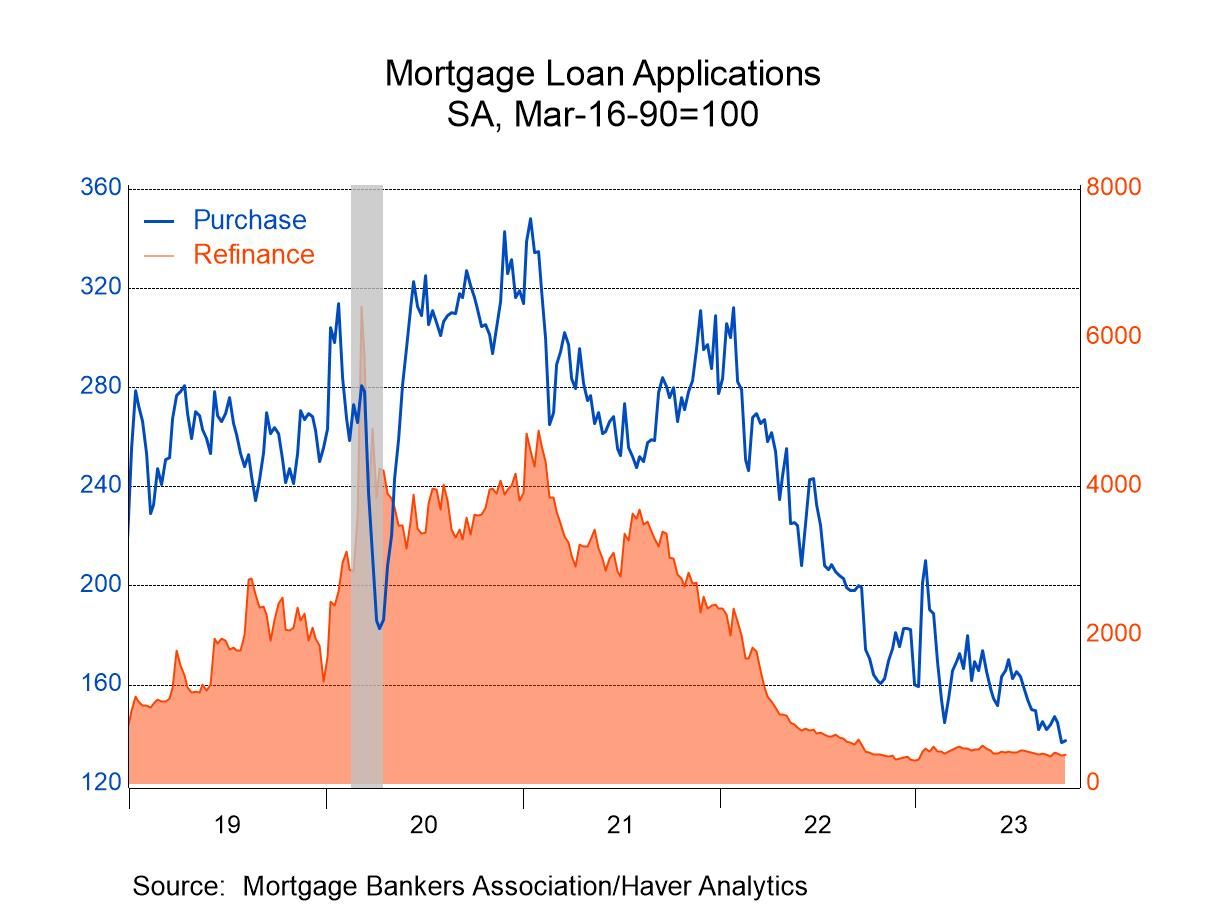

UK Finance released its figures as part of its Household Finance Review for the first quarter of 2024, exploring trends across household spending, saving, and borrowing. The review also noted that towards the end of last year, as mortgage rates started to reduce, there was a noticeable increase in the number of mortgage applications.

Mortgage applications graph

Mortgage applications graph

However, any sustained recovery has yet to materialise, as market expectations for a Bank of England base rate reduction have shifted to later in the year. The review said an “early stimulus” to mortgage demand this year “does not appear to signal a change from our forecasts – a picture of continuing, significant affordability constraints holding back activity through the year.”

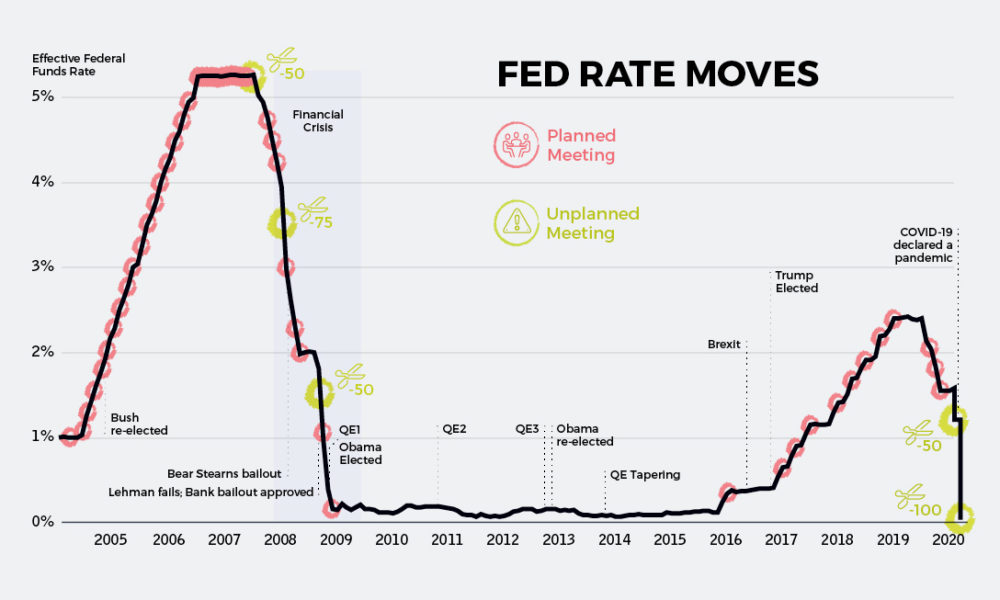

Interest rates graph

Interest rates graph

Eric Leenders, managing director of personal finance at UK Finance, said: “Some households were in a better place financially in the first quarter of this year, but we are not out of the woods yet. Cost-of-living pressures remain, and with 1.6 million mortgages due to come off fixed rates this year, there may be challenges ahead for some.”

Cost of living graph

Cost of living graph

Many lenders have signed up to a mortgage charter, which gives people who are struggling a range of options to suit individual circumstances. UK Finance’s review was released as financial information website Moneyfactscompare.co.uk said that, in the week running up to May 31, the number of fixed mortgage deals for borrowers with a 10% deposit fell from 700 to 696, while the number of fixed deals for those with a 5% deposit fell from 329 to 326.

Mortgage deals graph

Rachel Springall, a finance expert at Moneyfactscompare.co.uk, said: “The fact that a few lenders are withdrawing some higher loan-to-value products may raise eyebrows, but we are not seeing a mass exit. However, should more deals be withdrawn at higher loan-to-values, it may come as disappointing news to those who have a limited deposit, such as first-time buyers.”

Loan to value graph

The deals that have disappeared last week may well resurface, perhaps when re-pricing activity picks up in the coming weeks. Affordable housing is very much in short supply.

Housing supply graph

Housing supply graph

{kind=link}