Mortgage Rates on the Rise: What This Means for Homebuyers

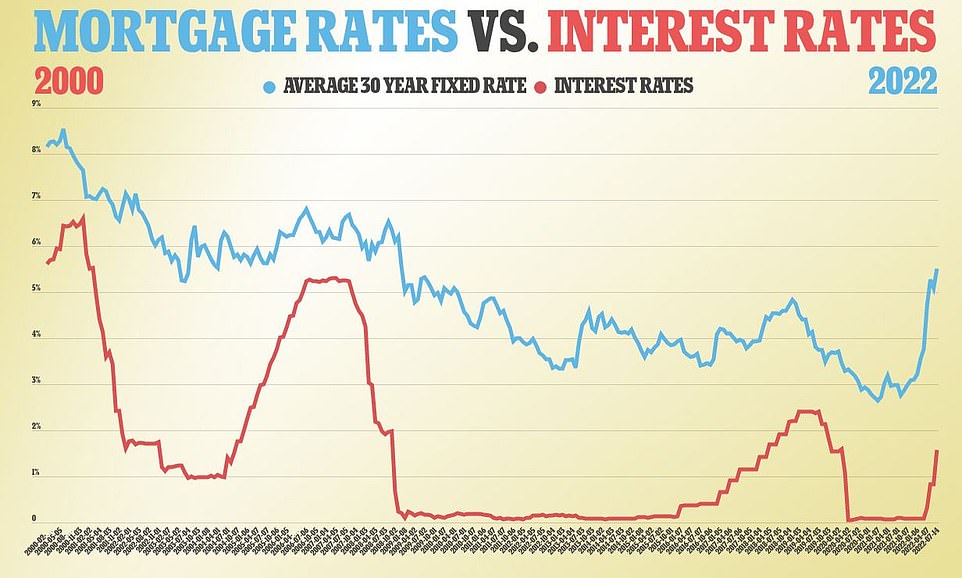

The UK mortgage market is experiencing a significant shift, with rates on the rise and anxiety among lenders. The average rate on a two-year fixed deal has increased to 5.89%, while rates for a five-year deal have risen to 5.34%. This upward trend is attributed to the uncertainty surrounding the Bank of England’s interest rate path.

UK mortgage rates are on the rise, making it challenging for homebuyers.

UK mortgage rates are on the rise, making it challenging for homebuyers.

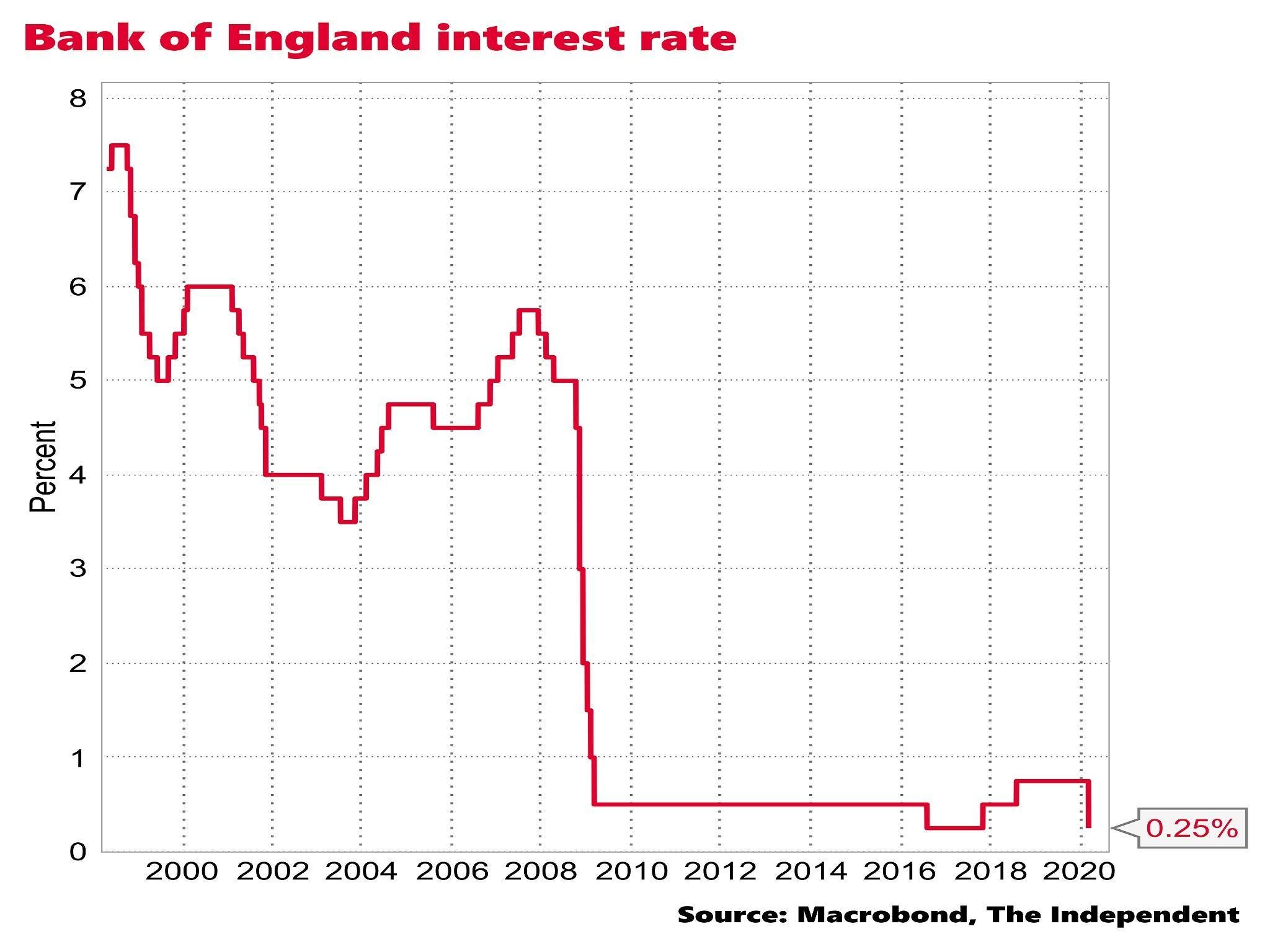

The Bank of England’s decision to leave interest rates on hold at 5.25% for the fifth consecutive time has led to lenders increasing their rates. This has resulted in a slump in house prices last month, with buyers becoming cautious amid rising mortgage rates.

Ranald Mitchell, director at Charwin Private Clients, notes, “Buyers are behaving cautiously at the moment, so the fall in prices in April comes as no surprise. The ebullience at the start of the year has been slowly eroded as mortgage rates have edged up.”

HSBC Mortgage Rates

HSBC has increased its mortgage rates, with the cheapest deal now standing at 4.48% for a five-year deal. The two-year option comes in at 4.83% with a £999 fee. These rates assume a 60% loan-to-value (LTV) mortgage, meaning buyers need to have at least 40% for a deposit.

NatWest Mortgage Rates

NatWest has lowered some of its mortgage rates, but the best rates available are 4.40% for a five-year deal with a £1,495 fee, assuming a 60% LTV. The two-year fix comes in at 4.77% online, with a £1,495 fee.

Santander Mortgage Rates

Santander’s five-year fix now stands at 4.35%, assuming a 40% deposit. The two-year fixed rate with a £999 purchase fee is priced at 4.78%.

Barclays Mortgage Rates

Barclays’ five-year deal for prospective homebuyers with a 40% deposit has increased to 4.47%. The two-year mortgage deal comes in at 4.84%.

Nationwide Mortgage Rates

Nationwide’s five-year purchase fixed rates start from 4.59% with a £999 fee for borrowers with at least 40% deposit. The equivalent two-year rate starts from 4.84%.

Halifax Mortgage Rates

Halifax, the UK’s biggest mortgage lender, has lowered some of its deals across a range of mortgages. The lender offers a two-year fixed rate of 4.80% with a £999 fee for first-time buyers.

Cheapest Mortgage Deal on the Market

As under 4% mortgage rates are no longer available, it’s becoming harder for prospective homeowners to secure a good deal. Santander’s 4.35% deal appears to be one of the cheapest rates available, but it requires a 40% deposit.

Mortgage rates are rising, making it challenging for homebuyers to find a good deal.

Given the average UK house price currently sits at £261,962, a 40% deposit equates to about £105,000. Borrowers would need to spread their home loans over more than 70 years to be able to afford the same mortgages on offer just two years ago.

There is, however, a new mortgage product that promises to help first-time buyers get on the property ladder with just a £5,000 deposit. Yorkshire Building Society is offering a deal that will enable first-time buyers across England, Scotland, and Wales with a £5,000 deposit to purchase a property valued at up to £500,000.

Will Mortgage Rates Go Down in 2024?

Mortgage rates have risen substantially as the Bank of England increased interest rates to a 16-year high to tackle inflation. Until now, the consensus was that interest rates have peaked, and 2024 will see the Bank start to cut rates as inflation eases. However, inflation slowed down less than expected, pushing City investors to cut their forecasts for how much the Bank of England will cut interest rates this year.

UK interest rates are on hold, affecting mortgage rates.

UK interest rates are on hold, affecting mortgage rates.

Traders are now pricing in just two interest rate cuts this year, compared to expectations of five cuts at the start of 2024. If the BoE only makes any cuts this year, mortgage rates will come down, but not as much as originally expected for 2024.

About 1.6 million existing borrowers have relatively cheap fixed-rate deals expiring this year. As mortgage rates continue to rise, it’s essential for homebuyers to stay informed and adapt to the changing market.

{kind=link}