Remortgage Market Sees Shift in Borrower Behaviour

Remortgage instructions decreased by 4% in April, according to data from LMS’ monthly remortgage snapshot. While the overall cancellation rate decreased by 16%, there were 9% more remortgages completed throughout the month. Pipeline cases decreased by 3% month-on-month, with 43% of borrowers increasing their loan size.

Remortgage market trends

The average monthly payment increase for those who remortgaged in April was £354.51, with 44% of those who remortgaged taking out a 5-year fixed rate product. 28% of remortgagers said that their main aim was to lower their monthly payments, while 25% wanted to release equity or borrow more money.

Regional Variations

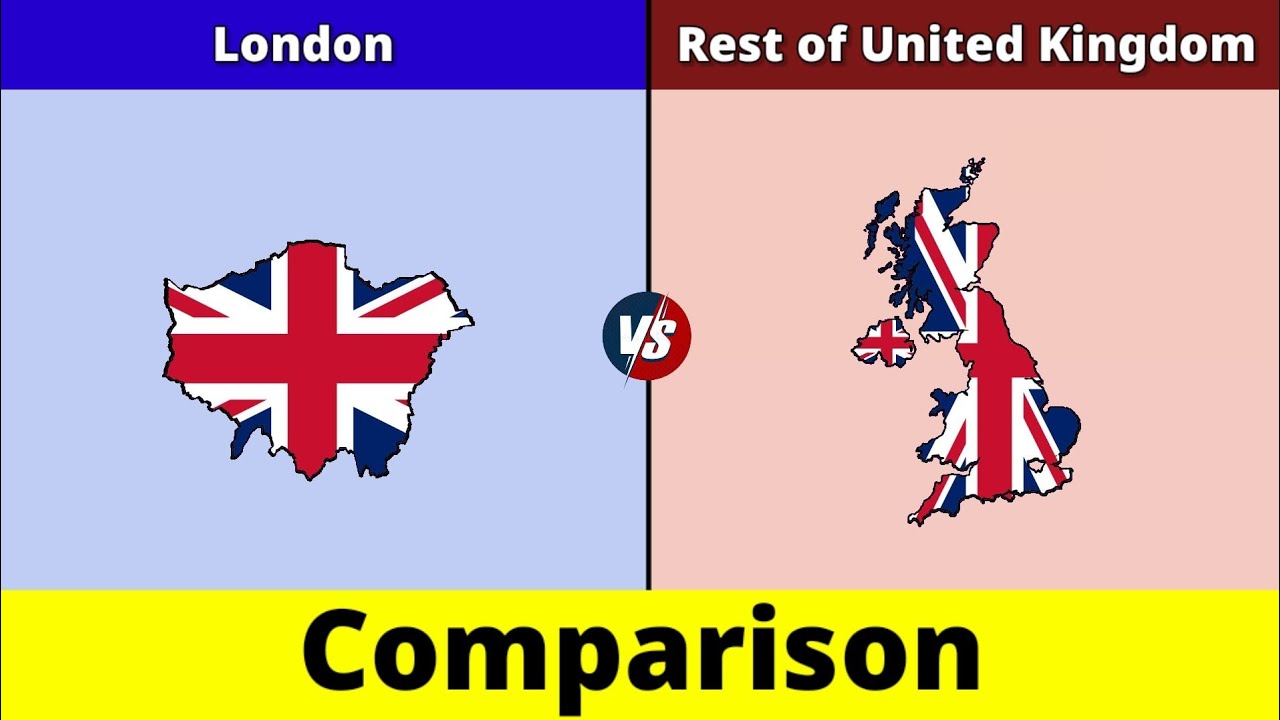

On a regional level, the average remortgage loan amount in London was £349,675, while the average for the rest of the UK stood at £173,597. This made remortgage loan amounts 101% higher in London than in the rest of the country. The longest previous mortgage length was found in the North West at 70.54 months (5.88 years), while the shortest was in East Anglia at 59.12 months (4.93 years).

Regional remortgage loan amounts

Regional remortgage loan amounts

Expert Insights

Nick Chadbourne, CEO of LMS, commented: “The key mortgage figures from UK Finance in 2023 showed an increase in product transfers (PTs) of 17.1% compared to those in 2022 – it is clear that the PT trend has continued into 2024. Whilst not as significant as April, we are heading towards another ERC spike at the end of July. Typically, this would mean an increase in remortgage instructions a few months prior; however, as is shown, we have experienced an atypical decrease in remortgage instructions month on month.”

“In other news, for the first time since November 2023, a 5-year fixed product has become the most popular choice amongst customers. Our data also shows that 73% of customers’ product choices are motivated by security and wanting to know how much to pay per month. Both metrics indicate that a critical driver for borrowers is wanting certainty of mortgage payments over the longer term; although the Bank of England suggests rates will reduce, borrowers are opting for potentially higher payments over a longer term to ensure they have that certainty.”

Nick Chadbourne, CEO of LMS

Shift in Borrower Behaviour

Chadbourne concluded: “Affordability and rates remain key factors, but are we now looking at a shift in borrower behaviour? Are borrowers deciding to tie themselves to the same lender for multiple product periods? The data certainly suggests so.”

Shift in borrower behaviour

Shift in borrower behaviour

{kind=link}