Rise of Ultra-Long Mortgages Puts UK Retirement Prospects at Risk

Homebuyers in the UK are increasingly being forced to take on ultra-long mortgages that stretch beyond their state pension age, posing a significant risk to their retirement prospects. According to recent data, more than a million mortgages with terms exceeding the borrower’s state pension age have been arranged in the last three years.

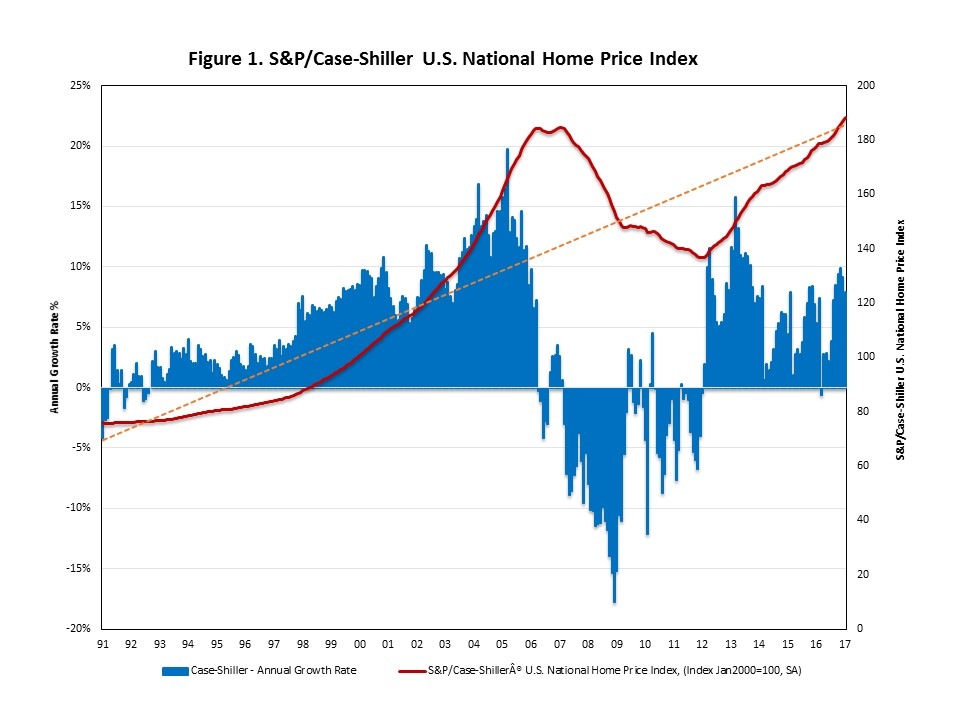

The UK housing market is becoming increasingly unaffordable for many.

The UK housing market is becoming increasingly unaffordable for many.

The data, obtained via a freedom of information request, shows that the proportion of home loans arranged to last into retirement increased from 31% in the final quarter of 2021 to 42% in the same period last year. This trend is particularly concerning among 30- to 39-year-olds, who are typically taking out their first mortgage. In this age group, 30,943 home loans were arranged to last beyond state pension age, with 39% of those granted in the last three months of 2023.

Mortgage applications are on the rise, but at what cost to retirement savings?

Mortgage applications are on the rise, but at what cost to retirement savings?

The figures are even more striking among 40- to 49-year-olds, with 32,305 new mortgages, or 57% of the market, arranged beyond typical retirement age. This compares to 42% in 2021. While older age groups are also taking on ultra-long mortgages, the numbers are significantly smaller.

Retirement savings are being put at risk by the rise of ultra-long mortgages.

Retirement savings are being put at risk by the rise of ultra-long mortgages.

The rise of ultra-long mortgages can be attributed to rising house prices and interest rates, which have made it increasingly difficult for people to afford homes. While arranging a mortgage over a longer period reduces monthly repayments, it can have devastating consequences for retirement prospects.

Housing market trends are changing, and it’s putting pressure on retirement savings.

Housing market trends are changing, and it’s putting pressure on retirement savings.

Former pensions minister Steve Webb, a partner at the pension consultants LCP, submitted the freedom of information request to the Bank of England after it reported that two in five borrowers had taken out loans that would run beyond state pension age. The Bank supplied figures for the final quarters of 2021, 2022, and 2023, showing all new residential mortgages issued in those periods.

Steve Webb, former pensions minister, raises concerns about the impact of ultra-long mortgages on retirement prospects.

Steve Webb, former pensions minister, raises concerns about the impact of ultra-long mortgages on retirement prospects.

The data highlights the need for borrowers to carefully consider the long-term implications of taking on ultra-long mortgages. With more than a million mortgages already arranged to last beyond state pension age, it is essential to address this issue to ensure a secure retirement for future generations.

Retirement planning is crucial in the face of rising ultra-long mortgages.

Retirement planning is crucial in the face of rising ultra-long mortgages.

{kind=link}